Greetings from Rome! Welcome to our CESIO edition. If you’re looking for a summary of the presentations and discussions at CESIO, sorry, we don’t do that here. You should have bought a ticket and shown up. It was an outstanding event, well produced and organized. Kudos to CESIO president, Tony Gough. Alex, Chantal and the rest of the team.

I’ll tell you about my experience there if you’re interested. I had the usual crazy title for my talk and once again the organizers kindly indulged me with a speaking slot to kick off the business track on Wednesday morning. Dinosaur eats Unicorn was the paper title that got folks in the room at 8.30AM after a late night prior at the gala dinner. Session chair, Felix Mueller, reminded me that he introduced me on my first occasion as a CESIO speaker in 2011. He also reminded the audience that, according to my last talk in Munich, 2019, I was friends with Debbie Harry (Blondie) and that my talks are invariably interesting, thought provoking and entertaining. So.. no pressure then. We kicked off with a snippet of Blue Öyster Cult (Godzilla – Dinosaur – geddit?) to ramp up the dopamine in the room and then got right into it. I won’t give you the whole talk here, because, again, you shoulda been there, but I’ll tell you that an early shock for the audience was the revelation that unicorns are mythical and in fact do not exist. Nonetheless, they got a good sense of how, P2, as a venture-backed startup was navigating the so-called valley of death with the aid of several large dinosaur companions. Fun stuff.

So – next section – the news. If you’re only here for the music, that’s all the way down at the bottom.

The News

So – as noted in prior blogs: Biomass Balance is all over the surfacants and ingredients industry. Simply; taking in a renewable feed to your cracker, instead of taking in oil or gas, is a de-fossilization (de-carbonization) of the supply chain more or less proportional to the mass of oil or gas input displaced by the renewable input. Nothing wrong with that right? The Balance part of it comes when you allocate a certain part of the input against a certain product output from the downstream chain that is sold to a certain customer. That customer then is seucre in the knowledge that his purchase of the product has caused a certain proportional mass of renewable input to be used and thus brought about real, measurable and traceable de-carbonization. Nice.

My other favorite publication (other than ICIS News of course, my partners and collaborators in conferences, blog and whatnot) is Cosmetics & Toiletries. They had this to say recently about a new entrant to the biosurfactants field. :

Indorama Ventures has unveiled Surfonic Bio, a line of biosurfactants that offers low toxicity, mildness and biodegradability benefits and is obtained by a sustainable process.According to the company, the line synergizes with other classes of surfactants and can be used as a primary or secondary surfactant in formulations. The Surfonic line contains specialty wetting agents, emulsifiers and dispersants.

Applications of products in the line, including Surfonic Bio 5000 (INCI: Not Provided) include:

- Facial cleansers, makeup removal, anti-acne products;

- Shower gel, liquid soaps and intimate hygiene soaps;

- Moisturizing skin care products; and

- Shampoos, conditioners, scalp care and deodorants products.

So, there you have it. No word on if another company is making the products. If readers know, then please get in touch.

It’s been a while since we had news from Unilever, once the tussle with Nelson Peltz was settled. Now, however we learn that they have a new CEO, Hein Schumacher. The UL website has the following to say about him:

Hein Schumacher was appointed as a Non-Executive Director of Unilever PLC in June 2022 and his appointment took effect in October 2022.Hein was announced as CEO of Unilever in January 2023, and he will take on the role on 1 July 2023. Hein is a global business leader with an excellent track record in the consumer goods industry. He was CEO of Royal FrieslandCampina, an €11bn business operating in over 40 countries – and with products sold in over 100 - from January 2018 to May 2023. During that time, Hein delivered significant portfolio and organisation change as part of transforming it into a more focused, growth-driven and sustainable business. Prior to his appointment as CEO, Hein was Royal Friesland Campinas’s Chief Financial Officer for three years.

Prior to joining Royal FrieslandCampina, Hein worked for H.J. Heinz for over a decade. In 2008 he was appointed Chief Strategy Officer, before moving to Heinz China in 2011 as its President and CEO. In 2013, he was appointed Executive Vice President of Kraft Heinz’s Asia Pacific Zone and led a successful turnaround of the business, which spanned China, Indonesia, India, Japan and Oceania. Earlier in his career, Hein worked in finance as Corporate Controller, Asia and Central America for Royal Ahold NV. He began his career at Unilever. Hein also has previous board experience, having served as Supervisory Board member of C&A AG up to October 2022. Hein holds a Masters degree in Political Science and International Relations from University of Amsterdam.

He is married, with three children. OK, so not a bad resume.

Shall we take advantage of this UL news, to feature one more photograph of Nicola Peltz, apple of UL gadfly Nelson’s eye? Yes, we shall. Here courtesy of Tatler, in garb somewhat in the theme of the first part of our music section below..

News from BASF regarding APG’s. You may remember at our 2022 Jersey City conference, the company touted the many benefits of this class of compounds, in a bit of a re-launth talk. Now comes the investment news excerpted below, from a press release the company sent to me recently.

BASF will expand its global alkyl polyglucosides production capacity with two expansions at its sites in Bangpakong, Thailand, and Cincinnati, Ohio. By expanding in two regions in parallel, BASF, the global market leader for APGs, can strengthen its position and serve customers even faster and more flexible from the regional supply points, while at the same time reducing cross-regional volume flows. The additional capacities are expected to come on stream in 2025. “With this investment, we will solidify our position as a leading supplier of APGs in all relevant industries”, said Mary Kurian, President Care Chemicals. “Both our customers and consumers around the world are aware of the importance of sustainable formulations. At BASF, we are committed to providing sustainable products with strong performance. This expansion will enable the future of bio-based and biodegradable surfactants worldwide by offering diverse applications for personal care and home care, as well as industrial and institutional cleaning and industrial formulations.”

“As the sole producer of APGs in North America, this expansion demonstrates our unwavering commitment to deliver innovative bio-based and biodegradable surfactants to our customers”, said Marcelo Lu, Senior Vice President, Care Chemicals, North America. “With this additional capacity we stand ready to help customers reformulate and meet the increasing consumer and regulatory demand for more sustainable solutions across the Care Chemicals portfolio.”

“The Bangpakong site in Thailand is an important production hub for BASF in Asia already. This new APG line, together with our existing APG plant in Jinshan, China, will enable short delivery times and business continuity for our customers to support the growth and the increasing consumer demand for bio-based surfactants across the continent”, said Agus Ciputra, Senior Vice President, Care Chemicals, Asia Pacific.

BASF currently produces APGs in Duesseldorf, Germany; Cincinnati, Ohio; and Jinshan, China. The investment to expand regional production capacities in Asia and North America is triggered by a growing global demand and complements the existing facilities.

[No word on the capacity; so maybe I should guess? My dim recollection is that the original Cincinnati capacity for APG was about 25,000 MT per year and this was subsequently replicated at two other sites, one in Dusseldorf and one in Jinshan, China. My guess then is that maybe they will add another 25,000 MT in Thailand and perhaps a 10,000 MT expansion in Cincinatti? A complete guess, which, if wrong, perhaps someone can correct me?]

Our friends at Galaxy Surfactants in India published recent financial results: They posted net profit of Rs. 90.53 crores for the period ended March 31, 2023 as against net profit of Rs. 106.21 crores for the period ended December 31, 2022. The company posted net profit of Rs.98.40 crores for the period ended March 31, 2022. The company has reported total income of Rs. 981.50 crores during the period ended March 31, 2023 as compared to Rs. 1084 crores during the period ended December 31, 2022. Galaxy Surfactants reported total income of Rs.1054.13 crores during the period ended March 31, 2022. For the Financial Year ended March 31, 2023, Galaxy Surfactants has reported total income of Rs.4455.09 crores as compared to Rs.3698.22 crores during the Financial Year ended March 31, 2022. The company has posted net profit of Rs.380.98 crores for the Financial Year ended March 31, 2023 as against net profit of Rs.262.78 crores for the Financial Year ended March 31, 2022.

And just as CESIO kicked off, ICIS reported that - - starting this quarter, BASF is gradually bringing additional alkoxylation capacity on stream at Antwerp, Belgium, and Ludwigshafen, Germany, to meet growing demand in Europe. The capacity increase, totalling more than 150,000 tonnes/year, is mostly part of the expansion of BASF’s ethylene oxide (EO) and EO derivatives capacity at Antwerp, announced back in 2019. In addition to alkoxylation, the expansion includes a second world-scale EO production line, including purified EO capacity. "With this expansion, we are strengthening our position in Europe and opening up important growth opportunities in the European market through a wide range of applications such as in the detergents and cleaners, automotive and construction industries," said Mary Kurian, president, Care Chemicals, at BASF. Financial details were not disclosed.

[Given market conditions, I would say this is needed]

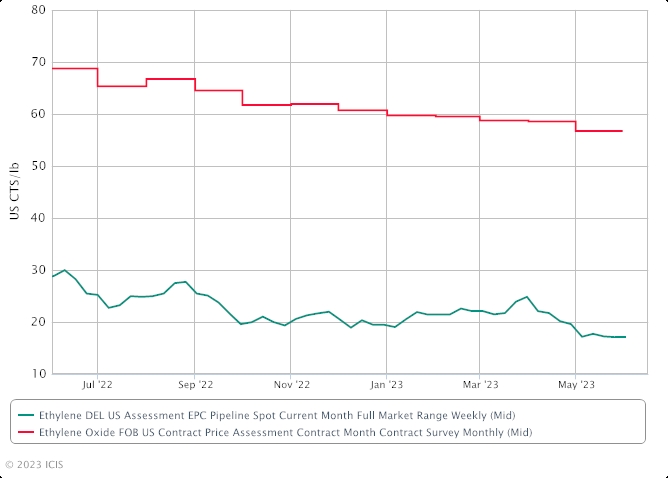

US May ethylene oxide (EO) contracts were assessed at 55.75-57.75 cents/lb ($1,229.06-1,273.16/tonne) end of May as upstream ethylene contracts continue to fall.

EO contract prices have declined for seven consecutive months, tracking an ongoing decline in ethylene contract prices as a result of lower production costs and spot prices. This is the lowest ethylene contract price since November 2020. Demand for EO and its derivatives continues to be weak as rising recession fears and ongoing elevated interest rates continue to deter discretionary spending. Additionally, consumers are spending more money on experiences, like travel, rather than on durable goods.

As expected, Swiss-based Clariant announced it has completed the sale of its global Quats business to Global Amines Company Pte Ltd. The agreement will be a 50/50 joint venture owned by Clariant and Asia's Wilmar. The transaction was signed 31 August 2022, and the sale of the business includes certain assets in Germany, Indonesia and Brazil. Quats are quaternary ammonium compounds, chemicals used for purposes including as preservatives, surfactants and as antistatic agents. Quats are used in a wide range of commercial, industrial and consumer products.

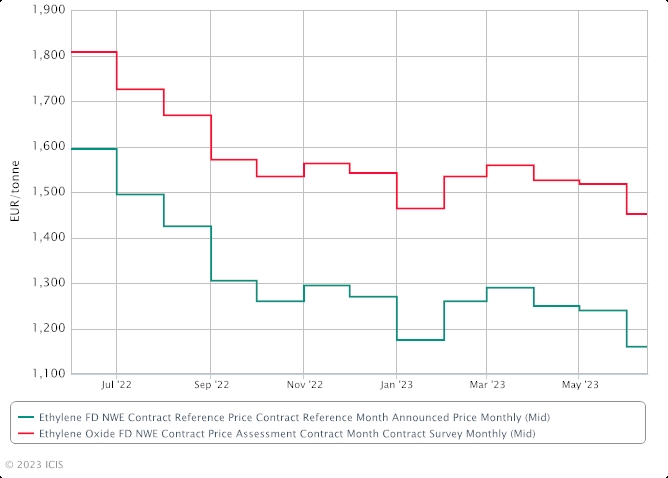

Similarly ICIS reports that, European ethylene oxide (EO) contract prices fall by double-digits in June, on the back of ethylene losses upstream. EO June contract prices were assessed at a €66/tonne decrease on both ends of the range, bringing prices to €1,383/tonne-1,521/tonne free delivered (FD) northwest Europe (NWE).

The European ethylene contract reference price for June has been set at €1,160/tonne, down €80/tonne from May. Upstream EO prices fell because of naphtha losses and continued low demand Demand remains low for EO derivatives as it failed to pick up as market sources hoped last month. Nonetheless, the pricing relief is likely to be welcome news for consumers particularly. Additionally, gas prices have also fallen to pre-war levels.

Meanwhile in Turkey, Univar Solutions has completed its previously announced acquisition of Turkish specialty chemicals distributor Kale Kimya, the global chemical and ingredients distributor said in an update on Thursday. Istanbul-based Kale Kimya offers a portfolio of beauty and personal care products, and home and industrial cleaning products, including surfactants, actives, emulsifiers, preservatives, UV filters, fragrances, polymers, conditioners, esters and emollients. The acquisition price or other financial terms were not disclosed.

More market weakness: ICIS notes that the Asian linear alkylbenzene (LAB) market remains weak with demand still in a low ebb. Buyers continue to expect further weakness in the near term and have pegged buying indications at a low level.

- Chinese domestic market declines

- Demand continues to sag

- Buyers expect weaker prices on raw material cost decline

The decline in Chinese domestic prices to yuan (CNY) 11,900/tonne DEL (delivered) this week, from CNY12,200/tonne DEL previously further dented sentiment across Asia.

“The Chinese LAB market looks likely to remain weak in June,” said a producer in China. Participants in Asia continue to expect a potential increase in Chinese exports should demand in the mainland fail to revive. Chinese suppliers have reduced export offers but lamented the weak buying interest in the region. Offers for spot cargoes were quoted at $1,450-1,500/tonne FOB (free on board) China but response from customers was lukewarm. Some buyers pegged buying ideas at around $1,450/tonne CFR (cost & freight) NE (northeast) Asia but sellers thought these prices too low, given the narrow margins they are experiencing now. LAB is an organic compound used almost wholly as an intermediate in the production of surfactant linear alkylbenzene sulphonate (LAS), also known as linear alkylbenzene sulphonic acid (LABSA). LAB’s main end market is the biodegradable detergents and other cleaners. In Southeast Asia, demand was also lacklutre with buyers citing low buying indications at under $1,500/tonne CFR SE (southeast) Asia. The recent availability of European lots at competitive prices took the wind out of the sails for the LAB market. Buyers started to ask for lower numbers, thwarting suppliers' attempts to sell material at around $1,550/tonne CFR SE Asia.

“Buyers’ sentiment is soft and they believe the market will grow weaker and hence their reluctance to buy,” said a trader in SE Asia. At the same time, the decline in raw material costs further dampened sentiment of players, with buyers pressing for even lower numbers for LAB. The wide buy-sell gap hampered trade although some sellers did lower offers in a bid to draw customers forward. Buyers, however, remain unconvinced and kept to the sidelines. Some sellers believe that buyers will continue to wait for the market to bottom out before stepping back in to pick up material.

Good news from Sasol. They lifted their force majeure on US linear alcohols and linear alcohol-based surfactants on 1 June. Sasol will maintain a sales control on some alcohol homologs until inventories are fully restored. Sasol declared force majeure on US Ziegler alcohols and derivatives following a 15 October fire at its US Lake Charles, Louisiana, plant. The company restarted production at 50% during November, as the fire impacted an area of the plant in which Sasol has redundancies.

Finally, In other Sasol news, this interesting article was published about their ventures group collaboration with Emerald Ventures. Worth a read as it’s relevant to their activities with Holiferm in Manchester.

The Music

If you’re new to the blog, this part comes at no-extra-charge and is completely voluntary reading and listening. On those rare occasions where a piece of music is compulsory listening for blog readers, it will be placed at the top, above the news section.

So, I’ve been impressed with both the quality and quantity of the output of French instrumental psychedelic group, King Weed. The album art (as it were) is redolent of a certain early 70’s ambience and is of a piece with the music, together pleasing two out of five senses. I found these guys, again, courtesy of the ever-helpful Youtube algorithm.

Come down this rabbit hole with me:

There is a lot more from them on the Tube. Let me know what you think..

Separately, I’ve been listening to a lot of Robin Trower. Great British blues guitarist. I remember, getting up early to watch Saturday morning re-runs of the Old Grey Whistle Test, back in England, which invariably featured interesting music, like this:

Is that not the absolute definition of a blues riff? Not sure what else to say..

And this

And this – the great Day of the Eagle

And then, I can’t wait much longer. Is there a more quintessential heavy rock blues song than this ? Two luscious guitar solos. Lyrics to break the hardest of hearts.

Lets’ end up with something a little more upbeat. One of our CESIO colleagues mentioned his fondness for The Stranglers and so this track I think is appropriate as it could indeed have been a soundtrack for the conference itself. I always liked the bit at the end. What was I hoping would change in 1977? Probably nothing more the endless pressure of O levels and A levels and tests and exams and such. Some revolutionary!

I really have to go now. This blog’s late enough already. If you are not satisfied with our service this summer, you can get in touch with your customer service representative and ask for a refund of your blog subscription price……

Until next month.